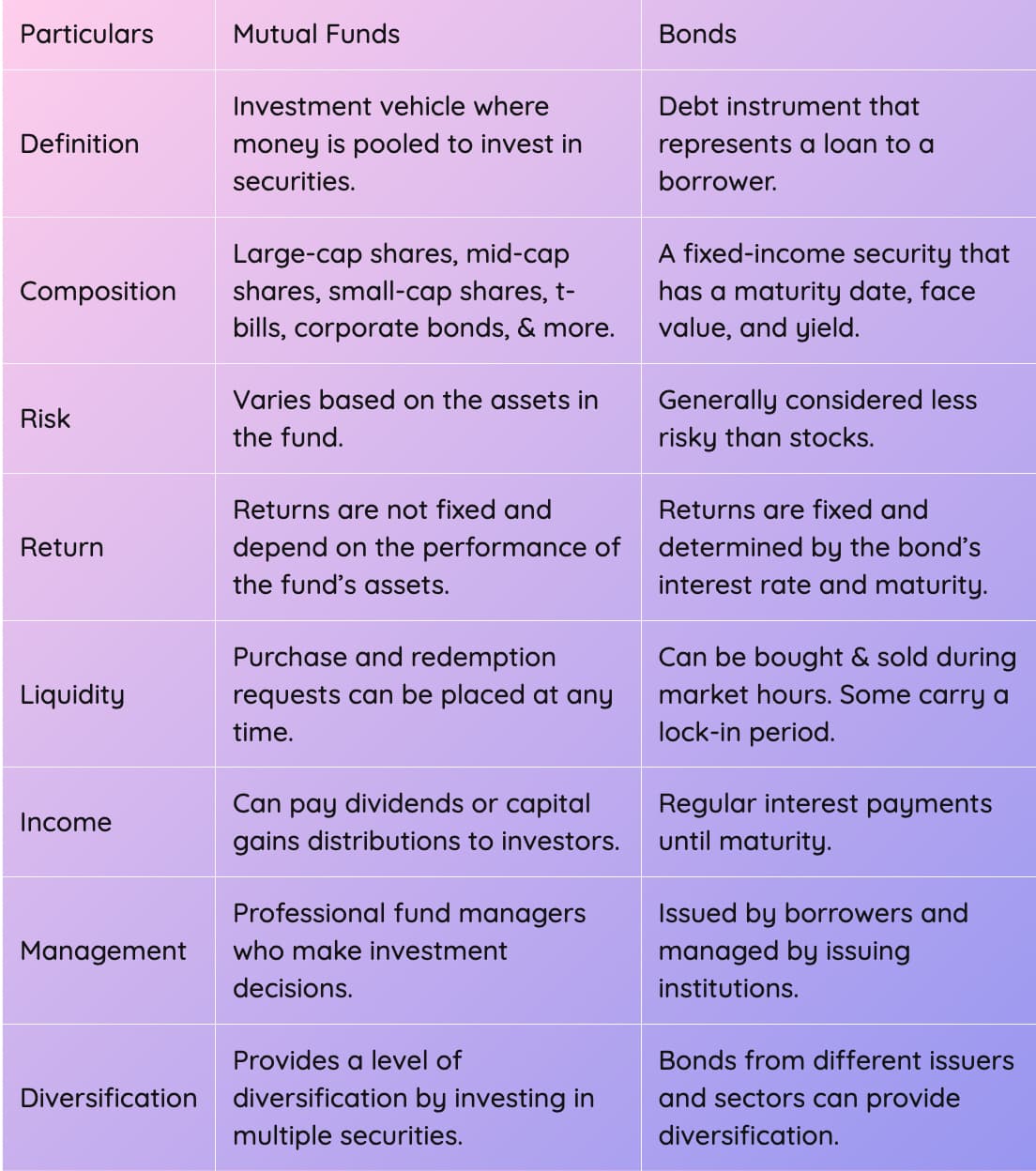

Mutual funds and bonds are prevalent investment options, each possessing distinct advantages and disadvantages. While both avenues hold the potential for profitable returns, they exhibit noteworthy differences

Personally, I feel the comparison would be more fair if we say “Debt Mutual Funds” vs “Bonds”, since equity mutual funds are a completely different asset and someone with a low risk profile would not even consider them.

For the longest time, this was a no-brainer because of the tax advantages that the former enjoyed. With indexation benefit on Debt MFs held for greater than 3 years, the effective LTCG (long term capital gains) was very good.

However, we all know that this no longer applicable since 1st April 2023 and all Debt MFs are now taxed as per your tax slab.

Now that both these investment avenues are mostly at par in terms of taxation, I would still go for Debt Mutual funds because of the following reasons:

Debt Mutual Funds can have any instrument in their underlying, not necessarily a debt instrument. For example, they can hold up to 35% of it’s underlying assets in equity. Considering my age and risk profile, this gives me greater freedom to choose a balanced fund.

Since I am accumulating my corpus and don’t need monthly interest payouts, Debt MFs makes more sense.

Of course, this is just my opinion and I’m sure there is a different segment for bonds, but I’m willing to hear more from others here!

Hey @shraddha thanks for tagging, ill share my insights. I would say both options have their merits.

Investing in stocks is relatively straightforward, but investing in Commercial Papers (CPs) of a company requires more in-depth analysis. It involves understanding how the company utilizes debt, assessing credit ratings, and evaluating the quality of assets that serve as collateral. Moreover, the debt market is less accessible to retail investors as, with most papers are privately placed with the institutions where they can get all of their funding needs. I generally opt for a debt mutual fund with a significant exposure to private placements rather than government securities. Additionally, only a fraction of these debt papers, such as Non-Convertible Debentures (NCDs) and Debt Segment (in BSE), are actively traded on exchanges. Personally, I keep a regular track of a few of these papers and make purchases when the YTM is attractive. Due to the segment’s limited liquidity, market dis-equilibrium do exist at times.

On the other hand, when it comes to investing in bonds directly, I choose to invest solely in Sovereign secured bonds, primarily G-Secs and T-Bills. This approach offers a dual benefit. Firstly, I can pledge these bonds and engage in options trading. Secondly, these bonds provide a fixed ROI of approximately 7.5% (in the case of G-Secs) and I can earn an additional 12-15% through options trading (mainly LEAPS).

Recently, I have also invested in SBI-AT1 Perpetual Bond (purchased via Exchange), which ensures a steady cash flow indefinitely.

I am not a great fan of mutual funds. I used to invest in ELSS for tax saving purposes only. With the new more attractive tax regime that compulsion is not there any more.

I prefer bonds if it has good liquidity and if it can be pledged to derive margin to facilitate my trading activity.

Hi @pavz Yes, we are building a product for bonds specifically where-in you can apply for these NCDs and also NCB Bidding for G-Sec, T-Bills, SDL’s, and SGBs. We are planning to roll this out in this quarter. However, incase you want to apply right now, you can use the NSE;'s goBID Portal. You need to register for the same using Dhan BOID and Bid directly.