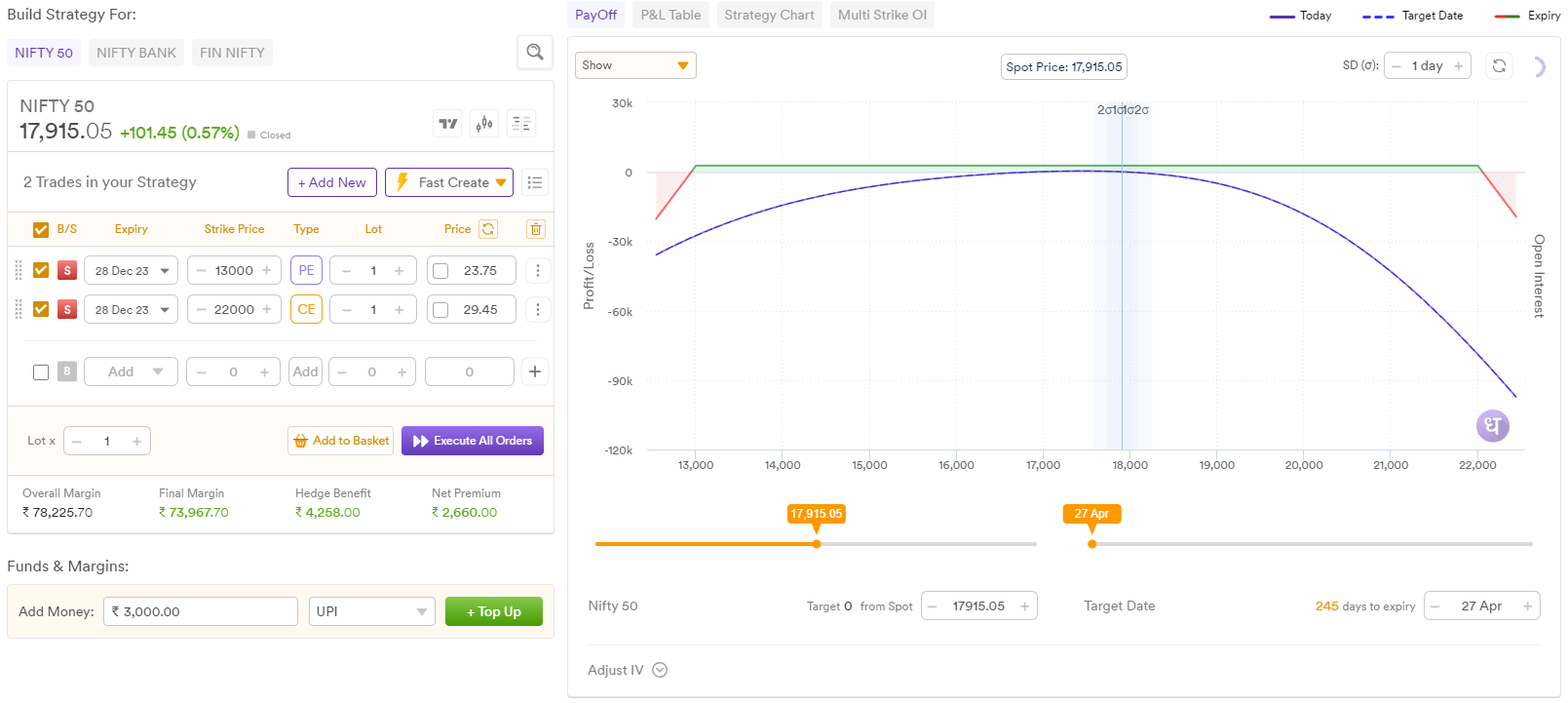

Strategy used: Strangle - Range depends on Risk Appetite and expected ROI

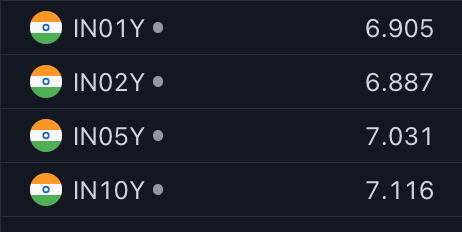

Mechanism: This strategy is mainly for those traders who don’t have much time to track the market and want to deploy a long term strategy. The underlying assumption behind this strategy is that NIFTY 50 will be between 13,000 and 22,000 until December 2023 expiry i.e. 8 months from now. Sell the 13,000 PE (LTP 23.75) and 22,000 CE (LTP 29.45). You will receive a net premium of Rs. 2660 and would need a margin of Rs. 75,000. Over the capital of Rs. 75000 the ROI would be approximately 3.5%. This when annualized would be equal to 5.25%. But this seems to be too less, even lesser than the existing FD rates (~7.5-8.0%). Now here is the catch. Deploy Rs. 85000 into G-Secs (post 10% haircut, you will get Rs. 76000 around as cash equivalent collateral value) which are eligible for pledging, the effective ROI on the G-Secs would be around 7.5%. Now compute the total annual return of the strategy - 5.25% + 7.5% ~ 12.75%.

Many HNI investors and Traders have been using this strategy to gain alpha. Depending on your risk taking appetite, you can adjust your strikes.

Disclaimer: Trading and investing in the securities market carries risk. The Content is for entertainment and informational purposes only and you should not construe any such information as investment, financial, or other advice. Data and information is from publicly available sources. Please do your own due diligence or consult a trained financial professional before investing or trading. Don’t take this post as investment advice, it’s purely meant for educational and entertaining purposes only.

Playing devils advocate again. Pardon me for the same.

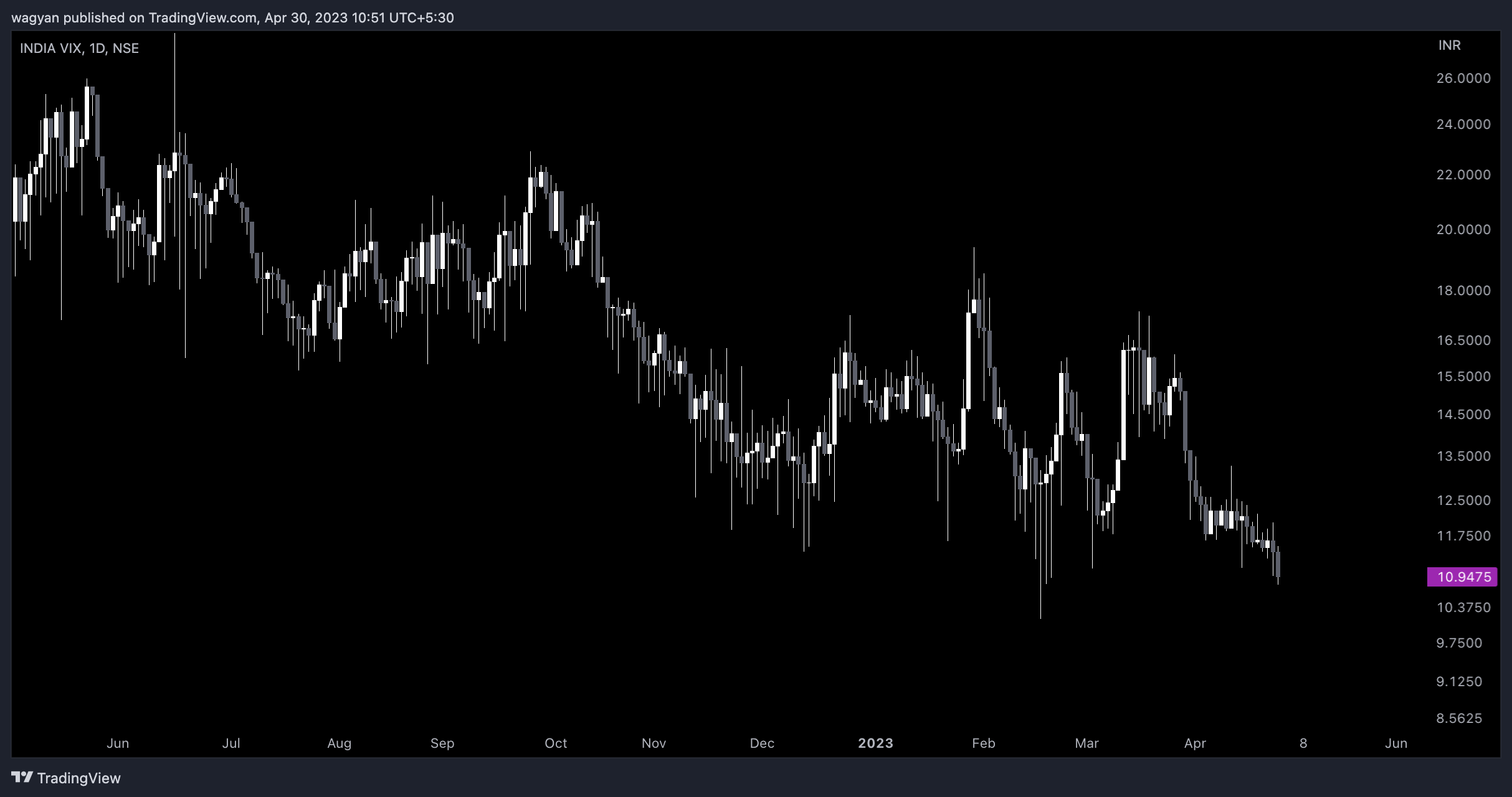

Wouldn’t the margin required increase with market movement on either side (which can be wild from MAY-DEC) ? So if someone just starts with 76000 after pledging just Rs.1000 is just not enough cushion.

@t7support Definitely the margins would shoot up for any high volatility event. Since the legs are wider, the impact will be lesser comparatively. Having said this, trading in any option strategy is “risky”. It looks easier to deploy any strategy but “fire-fighting” skill is quite intuitive in any strategy.

Will be talking about strategies with absolutely ZERO risk - like the Short Box Spread / Long Box Spread and how “Banks” have an edge over this to fund their lending business later in this series.

@t7support Firefighting strategies vary based on risk appetite and market experience, and there is no one-size-fits-all approach. Consequently, seasoned traders tend to focus on a single strategy and become experts in it rather than using multiple strategies.

Now for the strategy mentioned above, fire fighting can be done as: If the market moves sharply in one direction, traders can book profits on the other leg and wait for the market to consolidate. With the profits, they can either wait for further consolidation or purchase a hedge to limit losses on the extreme side. If capital permits, they can set up a new strangle with new strikes after consolidation.

Based on the deployment, the annualized ROI would be 5.25% for a duration of 8 months. However, there is a catch: if the premium erodes quickly and results in a better ROI within a few days or months, traders can opt to book their profits and switch to the next set of strikes. The goal of the trade is not to hold for the full 8 months but to generate alpha above the risk-free rate.

Excellent focus on detail - this is commonly referred to as “strategy optimization”. However, it’s worth noting that G-Sec payment frequency is semi-annual and interest payment dates may differ from security to security. Ideally, for this strategy, the G-Secs would pay interest twice within the 8-month cycle. It is commonly assumed that G-Secs or any underlying collateral with a fixed ROI will be held indefinitely.

@amit Liquidity is a matter of exchange. So on NSE / BSE / NDS-OM, the liquidity may vary. However, BSE and NSE would most likely have the same liquidity due to same participants. However in NDS-OM, only specific entities are allowed to bid and the minimum ticket size is Rs. 5 cr.

@amit Yes they do. An increase in interest rates can lead to a decrease in bond prices, and vice versa. This is due to the anticipation of new bonds being issued with higher yields, which makes existing bonds less appealing to investors. Nevertheless, if an investor holds a bond until it reaches maturity, the interest rate becomes irrelevant.